Regardless of whether you decide to outsource this aspect of your business or take a more DIY approach, there are a few things you need to be aware of when it comes to small business bookkeeping and accounting.

From establishing a business bank account to preparing for tax season, knowing the basics around the financial side of your operation can make your life a lot less

Set Up a Business Bank Account

Setting up a separate business bank account is the very first step toward

Not only does it make it much easier to keep track of your

It’s a good idea to have two types of accounts:

Checking: For business expenses like inventory, travel, shipping costs, packaging supplies, etc.

Savings: For stashing away profits and a percentage of your earnings for tax time.

When choosing a bank for your business, be sure to examine their different fee structures, balance requirements, and, for convenience, proximity to where you live. Some state banks offer free business bank accounts, but be sure to read the fine print.

Also keep in mind integration. If you’re going to be tying your business accounts to an accounting software, know that some smaller, local banks do not have the ability to integrate with these tools.

Before you go to the bank, make sure you have the required documentation with you, such as your:

- established business name

- tax ID

- personal identification.

Tracking Your Expenses

Next, you’ll want to determine how you’ll document your business expenses. This will help you keep a close eye on your margins and

Part of this means keeping your receipts and invoices organized. Be sure to keep receipts incurred from:

- Office expenses: what percentage of your home you use for business, or if you have an external office, receipts related to that expense

- Mileage or Vehicle expenses: You can deduct the annual mileage you put on your car for business travel (you’ll get a

state-mandated rate), or you can deduct a percentage of your total annual vehicle expenses (like oil changes, gas, etc.) - Travel: Hotels, food, and transportation costs from your business travel

- Meals/Entertainment: Business meetings for lunch, for

example–just be sure to note who you met with on the back.

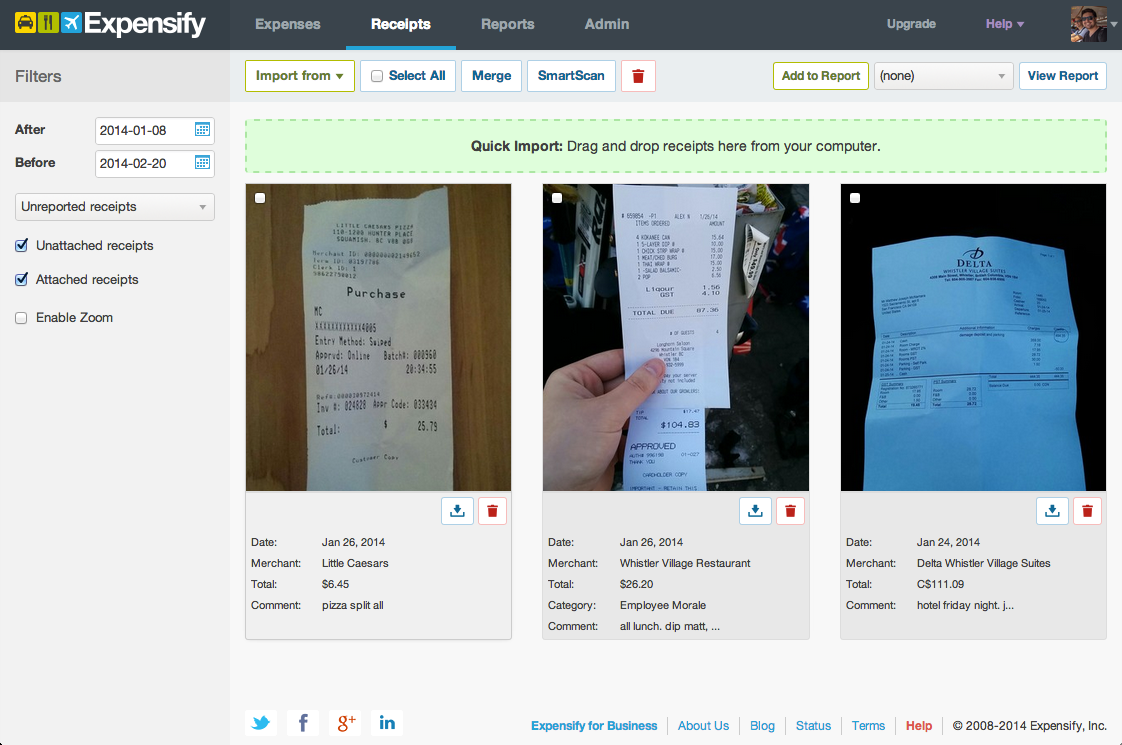

Documentation is essential for reliable

Image source: Expensify

To make this process a little bit simpler, you can take some proactive steps for documentation and storage. Consider the following tips:

- Keep a mileage log in your car so you can document miles traveled (and your destination) right away. A simple monthly planner works well for this.

- Keep a small accordion folder in your car or travel bag with sections marked for different types of receipts. This reduces the risk of them getting damaged or lost during travel.

- Once a month, check your receipt totals against your bank statement to make sure there are no discrepancies.

If you can take these steps toward accurate

Bookkeeping

Next, let’s talk about the bookkeeping.

Bookkeeping is the daily process of recording business expenses and transactions and reconciling them with bank statements. Unlike accounting, which looks at the numbers from a more zoomed out perspective for analysis, this part of the process is all about ensuring correct documentation.

There are a couple of different ways you can approach it:

- Work with a local bookkeeper/accountantwho handles it for you.

- DIY approach, which means using a spreadsheet or

cloud-based solution like Wave.

The right option for you depends on your bandwidth and ability. If you’re intimidated by this aspect of your business or simply don’t have time to devote to

- Accounts receivable and payable: What customers owe you, as well as what you owe to others

- Revenue and expenses: All transactions, including sales and costs associated with doing business

- Inventory: Detailed breakdown of quantities of stock, dates purchase, dates sold, etc.

It’s important to keep your books as accurate and

Understanding Your Tax Requirements

For many small business owners, the tax side of the business can be pretty intimidating. But with the right amount of saving and careful bookkeeping, it can actually be quite simple.

For the

If you make more than $1,000 per year, you’ll be required to make estimated quarterly tax payments. To calculate your quarterly payments, it’s a good idea to refer to last year’s filings as a guide if your business has stayed the same. If not, you’ll want to estimate your expected income minus deductions for the year. If you’re in the US, you’ll complete a

Overall, you’ll want to plan on setting aside a chunk of your earnings for tax time.

How much? A safe range is

Monitor Key Numbers

While you’re completing your bookkeeping work, you’ll want to do some analysis to monitor key numbers and to look for trends and patterns that can help you improve the business. Some key performance indicators to keep an eye on include:

Gross margins: This percentage will help you monitor your margins and get a firm grasp on how much you’re actually earning from your products. To calculate gross margin, use the formula: Gross margin (%) = (Revenue — cost of goods sold) / revenue

Monthly sales: Look for patterns that help you spot slow months and busy months. Use this data to inform your marketing and advertising strategy.

Marketing ROI: Keep track of the return on investment from your different marketing efforts to find out which channels and platforms are producing the best results. Moving forward, spend more on the channels that are delivering the highest returns and cut out the

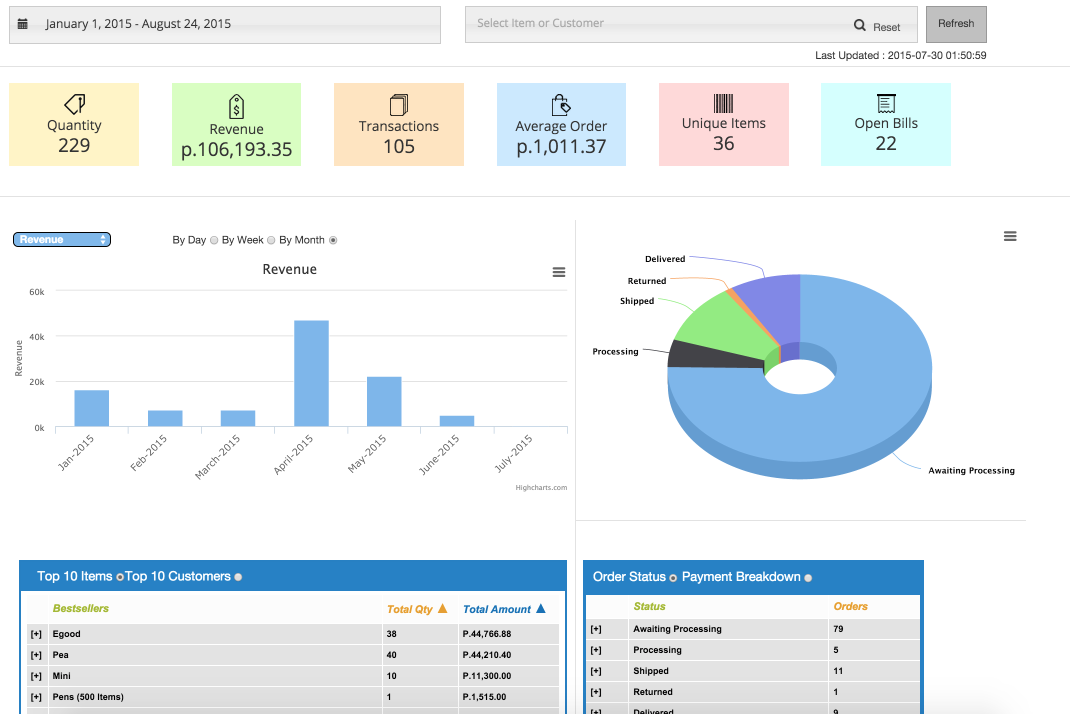

The good news is that Ecwid has detailed sales reports built into the platform, as you can see below:

Just remember: The numbers don’t lie. Refer back to these key figures when evaluating which products to

Small Business Bookkeeping & Accounting: Easier Than You Think

With the right financial information and a stellar product, you can grow a thriving small business in no time at all. If you’re doing the

Want more content on the financial side of your small business? Check out:

- Successful Small Business Ideas

- How to Start a Small Business

- Loan Options for Small Business

- How to Get a Grant for Small Businesses

- How to Compete With a Large

E-commerce Business as a Small Business - Running a

Woman-Owned Small Business - Marketing a Small Business Online and

In-Person - How to Promote Your Small Business Locally

- Taxes for Small Businesses Made Easy

- Small Business Bookkeeping and Accounting for Ecommerce

- Websites for Small Businesses

- How to Start a Small Farm Business

- How to Start a Small Food Business

- What is Petty Cash