Pricing is one of the most important considerations for any business. How much you charge for a product directly affects how much you can sell. Getting the pricing right can result in massive revenue boosts.

In this post, we’ll look at some strategies how to price your products using proven theories. You’ll learn about pricing science, statistical models, and pricing optimization based on the psychology of pricing products.

What is Pricing Science?

To put it into a tweetable sentence, pricing science is the use of statistical models and competitor analysis to create a pricing strategy.

Pricing science owes its origins to the deregulation of the airline industry in the late 1970s in the US. Airlines offer a

This is the reason why ticket prices keep changing depending on when you book your flight.

In terms of management theory, pricing science forms a part of yield management. It is an important enough aspect of business that most

Large businesses often have dedicated professionals whose sold job is to figure out the best price for the company’s products. To forecast demand, they use complicated equations that look something like this:

![]()

Terrifying, right? But as you’ll learn below, getting the pricing right is crucial for your business. The good part is, you don’t have to resort to equations like the one above to get this right.

The Pricing Process

It’s a simple fact of economics: as prices go up, demand goes down.

Your job as a business owner is to find the sweet spot between price and demand.

This equation can be represented as a curve, called Demand Curve:

In this scenario, your revenue would be a function of Total Purchases x Price of Each Product. This can be represented as a rectangle on the graph:

The sweet spot between price and demand would be the largest rectangle you can draw within this graph:

Of course, this is an oversimplification, but you probably get the idea — to get the pricing right, you need to find the median between price and demand.

Pricing Your Products: What Not to Do

Most businesses follow a rather simplistic pricing process called the Three C’s of pricing. These are:

- Cost: The total cost incurred in manufacturing the product. Price, thus, is cost + profit margin.

- Customers: What customers are willing to pay for the product. Usually found out through customer surveys.

- Competition: What competitors are charging for their products.

On paper, this sounds good enough. After all, if you take your cost, customers and competition into account, you should be able to arrive at an agreeable price.

In reality, this strategy fails more than it succeeds. Some reasons include:

- Costs can change depending on availability of raw materials. They can also change depending on the scale of production.

- Cost based pricing discounts the actual value you provide to customers. It also doesn’t take into account intangibles like brand value, customer demand, etc.

- Your competitor might be underpricing its products to gain market share.

- Customer surveys to determine prices are sketchy at best. What a customer is willing to pay theoretically on paper, vs. what they pay with actual money can be very different.

And so on. The tried and tested model seldom works. This is why you need to adopt a pricing strategy that takes customer psychology, statistical models, and demographics into account.

How to Choose the Right Product Pricing Strategy

A

1. Adopt Demographic Based Pricing

A cost or competitor based pricing model fails because it does not take customer demographics, product value or brand value into account.

To combat this, adopt a

For example, if you were selling jeans to rich celebrities, you can charge hundreds of dollars per pair of jeans. Instead, if your target market was

To make this possible, you need the following demographic data for your target market:

- Average income: Higher income means higher price tolerance.

- Gender: Men buy, women shop

- Location: Upscale location equals higher disposable income (not very useful for

e-commerce). - Education: Education has a positive correlation with income. More educated buyers, thus, can be charged more.

You can quantify demographic factors by taking into account their impact on sales (say, if average income is over $100,000, income gets a factor of 2, if less than $100k but over $50k, it gets a multiplying factor of 1, etc.).

With this you can use a custom formula to calculate the price. Obviously, this formula should be based on statistical analysis, but something as basic as this can work:

Price = (Cost of production * demographic factors) + profit margin — customer acquisition cost.

2. Adopt Dynamic Pricing

In 1969, Frank Bass, a professor at the Graduate School of Purdue University, developed a model for quantifying the adoption of a new product. This model, called the Bass Diffusion Model, gave a simple equation for how people come to use a product in a marketplace.

Without going all mathematical on you, this model essentially divides consumers into two groups:

- Innovators: These are the early adopters who try out new product and tell others about it.

- Imitators: These are people who start using a new product after it has already gained some traction, often after recommendations from innovators.

The number of innovators and imitators peaks after some time. Graphically, this can be represented as follows:

You can apply this model to most successful products — physical or digital.

For example, Facebook’s innovators were college students who first signed up for the service. Later, imitators jumped aboard when Facebook opened its doors to everyone.

The question now is

Even though the Bass Diffusion Model describes the adoption of new products, it is also widely used in pricing.

The idea is simple: you can maximize revenues from each customer by basing your price on a generalized Bass Model curve.

Graphically, we can represent it as follows:

In other words, you can:

- Price the product

low-moderate to attract early adopters. Make sure it’s not too low, else you won’t be able to increase prices later, and will affect value perception among late adopters. - Increase prices once adopters have become accustomed to the product. Alternatively, you can increase revenues through

cross-sells and upsells. - Decrease prices later in the customer life cycle to increase customer retention

Thus, your prices are never truly static but keep on changing along with the customer’s journey.

This is a powerful concept that removes the pressure to get the price just right. Instead, it forces you to adopt a dynamic product pricing strategy that is dependent on customer behavior.

Simple, but useful.

3. Increase price inelasticity

Price Elasticity of Demand, or PED measures changes in the demand for a product with changes in its price.

- If the demand decreases with increases in price, the product is elastic.

- If the demand remains the same regardless of price changes, the product is inelastic.

There are two methods to determine the price elasticity:

- Survey a sample audience from the target market. Ask them how their purchasing habits change with price.

- Study historical records to understand demand changes against price.

You can then calculate the price elasticity with a simple formula:

PED = % change in demand / % change in price

This usually yields a negative score (since demand typically goes down with price). For example, if you increase the price by 50%, the demand decreases by 100%. The PED, thus, is:

PED =

In rare cases, demand remains the same or actually increases as prices increase. This either happens in a bubble, or for commodities such as oil or luxury goods.

How does elasticity affect a company’s pricing policy

Price elasticity essentially gives you an understanding of how customers will react if you increase your price.

This is a function of three things:

- Scarcity: If a product is perceived to be scarce, it can command higher prices without a

let-up in demand. - Value: If the product delivers a lot of value (or is perceived so by consumers), you can increase the price without affecting demand.

- Brand: A brand perceived as a rare, luxurious or premium brand can command higher prices without a slip in demand. In some cases, demand can actually increase with prices. Such products are classified as Veblen goods.

Luxury products typically use brand perception, value perception and scarcity (real or artificial) to sell products at high prices.

One of the best examples of this can be seen with diamonds.

Diamonds are notably expensive and prized commodities. This high price tag comes from an assumption that diamonds are rare. Since there is very limited amount to go by, businesses are right in charging more for the product.

However, study after study has shown that diamonds are not only not rare, but even abundant.

Businesses that deal in diamonds, such as De Beers, are able to command top dollar for their products by creating artificial scarcity and aggressive marketing.

For instance, gifting engagement rings as a tradition was in steep decline after the First World War. Seeing the sharp fall for its product, De Beers launched an aggressive marketing campaign that emphasized how diamonds are forever — like the bond of marriage. The campaign was successful, and a practice limited to a select group of people suddenly became the established norm across the country.

All this marketing and positioning has turned diamonds into a largely inelastic commodity. It’s prices have steadily increased:

At the same time, demand has followed a similar curve:

The diamond industry managed to do this by:

- Controlling supply and creating an artificial scarcity of an otherwise abundant resource.

- Improving the brand perception of diamonds by positioning them as forever and a symbol of love.

- Improving value perception by emphasizing the toughness of diamonds and their heirloom status (a strategy frequently used by watch brands).

This aggressive positioning has helped turn diamonds into an inelastic product where consumers have a high tolerance for price changes.

How to Position Your Product

As a small business owner you can adopt several tactics to position your product for higher prices (without affecting demand):

- Focus on the craftsmanship involved in the manufacturing process. Watch brands do this phenomenally well. You can charge exponentially higher prices by becoming a Veblen product.

- Price higher — people often equate higher prices with better quality.

- Tell a story about the product’s design, creation and origins. Storytelling has been scientifically proven to improve sales. Retailers such as Woot and the J Peterman catalog do this for individual products. Others such as American Giant weave a story about the brand itself.

- Get better product design. Research shows that better designed products are perceived to be of a higher value by consumers. Even if the function remains the same, better form can improve your sales.

- Improve website design. Strong website design improves conversion rates as well as value perception for the product being sold.

Product positioning is a whole new topic altogether, but the above should give you some ideas to get started.

4. Follow Psychological Pricing Principles

Lastly, you can improve sales and conversion rates for your products by framing the prices based on consumer psychology principles.

There are a number of tactics under this category. Four such tactics you can use right away are:

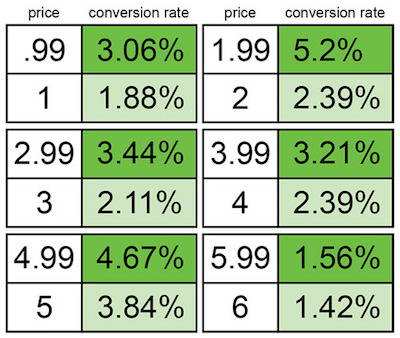

I. Use charm pricing

Charm pricing involves ending a price in 9 or 7 instead of the nearest round number.

It is one of the most widely used pricing strategies. Studies indicate that customers tend to focus on the numbers before the decimal point when they read a price.

Thus, even though there is just a $0.01 difference between $10 and $9.99, customers are more likely to view the latter as lower priced than the former.

In fact, a study by Gumroad, a payment processor, shows that products that use charm pricing often sell 2x more.

II. Increase prices marginally

If you must increase the price of a product, make sure that the changes are marginal but frequent. Customers should barely register the change. Jumping from $12 to $15 will trigger resistance. But gradually increasing price from $12 to $13, then $13 to $14 and so on over 12 months won’t invite as much scrutiny.

In experimental psychology, this idea is called

III. Split price into smaller units

A great way to increase sales is to split the price into smaller installments. For example, instead of asking customers to pay $100, you can ask them for five installments of $20 instead. Even though the actual price remains the same, customers perceive the latter to be smaller since it reduces the sticker shock associated with the price.

This strategy is frequently used by subscription products that give discounts for annual plans, but frame the price in monthly, not annual billings.

This way, even though the customer is being billed annually, he perceive the price to be lower since it is split into smaller monthly payments.

IV. Separate shipping costs from the price

When pricing your product, it’s important to keep the shipping and handling costs separate from the main product price. Else, you risk customers thinking that the total cost is actually the product price.

For example, if the product price is $30, and shipping costs $10, offering $40 as the total price will make the customer believe that the product itself is priced at $40.

Most retailers follow this strategy. For example, Amazon clearly mentions the shipping and handling costs separately.

Conclusion

Getting the pricing right is one of the harder challenges you’ll face in your business. By adopting scientific,

Key Takeaways

- Use product positioning to increase prices without affecting demand.

- Frame prices using psychological principles to maximize potential revenues

- Base prices on demographic data.

- Adopt dynamic pricing that changes along with the customer’s journey.

- How to Price Your Products? A Science Backed Answer

- Three Pricing Models You Can Implement in Your Online Store

- Penetration Pricing: The Winning Strategy to Get Customers Quickly

- How to Calculate Price Elasticity of Demand